For nearly two years, the U.S. equity bull market has been driven largely by a handful of mega-cap technology names: the "Magnificent Seven" (Apple, Microsoft, Alphabet, Amazon, Meta, Tesla, and NVIDIA).

Together, they have dominated index performance, particularly within the Nasdaq 100 and S&P 500.

Yet as the rally continues, a pressing question emerges: is the bull market finally broadening to include more sectors and companies?

Concentration Risk: The Rise of the Magnificent Seven

Since October 12, 2022, the Nasdaq 100 has surged nearly 118%, far outpacing other major indexes.

The market capitalization of the Magnificent Seven has doubled its share of the S&P 500 from 16% to 32%.

While this concentration has amplified gains for investors heavily weighted in these companies, it also poses systemic risks.

A stumble in just one or two of these names could have outsized effects on the broader market.

This level of concentration echoes the late 1990s tech bubble, when a small cluster of stocks drove market enthusiasm.

However, there are key differences today: earnings power.

Information Technology and Communication Services together account for roughly 37% of the S&P 500’s forward earnings – significantly more than their 24% share at the peak of the dot-com era.

MidCaps and SmallCaps: Valuation Opportunities

MidCap (S&P 400) and SmallCap (S&P 600) stocks have lagged their LargeCap peers, especially the S&P 1000 SMidCaps.

Although these groups occasionally outperform during periods of renewed optimism or Fed easing expectations, they have not sustained leadership since the mid-2010s.

One reason: forward earnings growth has been sluggish, still meandering below 2022 highs.

That said, the valuation gap between SMidCaps and LargeCaps is wide.

Investors willing to take on more risk may find opportunity in these less-loved sectors, particularly as expectations rise for rate cuts in late 2025.

If earnings momentum broadens, the setup could favor rotation.

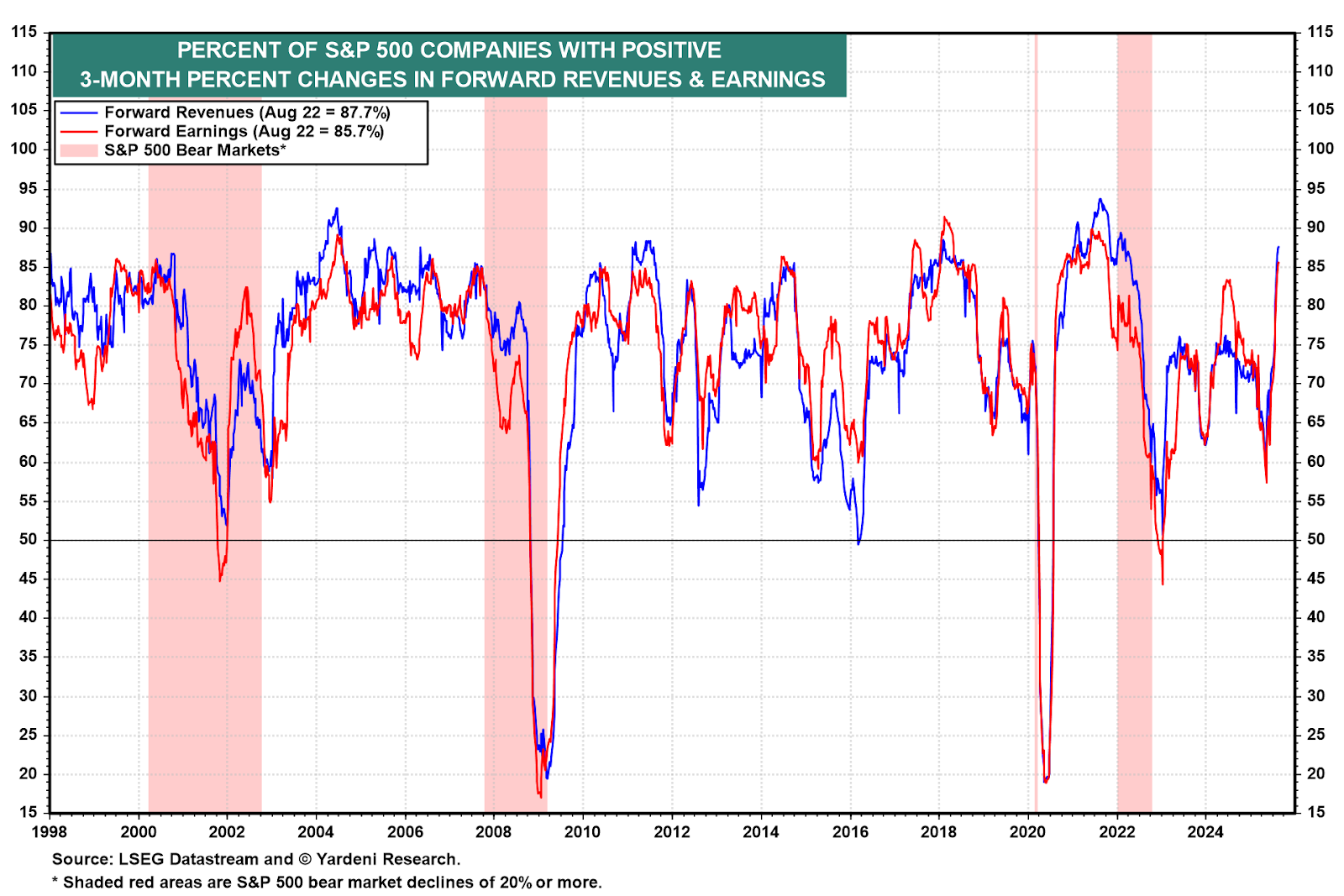

Encouraging Signs of Breadth

Recent weeks have shown a meaningful increase in the percentage of S&P 500 companies with positive forward revenue and earnings revisions.

This broadening of earnings growth suggests the rally is not solely dependent on the Mag-7.

While mega-cap tech remains the dominant force, Industrials, Financials, and certain Consumer sectors are beginning to contribute.

Market breadth is often a critical indicator of the durability of bull markets.

Narrow rallies tend to burn out quickly, but broad participation lays the foundation for sustained gains.

If more of the "S&P 493" continue to show earnings improvement, 2025 could see a healthier balance in leadership.

The Fed’s Role and Melt-Up Risks

The Federal Reserve’s policy path remains a wildcard.

Markets expect a rate cut in September 2025, reminiscent of the 1998–1999 period when a Fed easing cycle helped fuel a spectacular melt-up in tech stocks.

While today’s valuations are stretched, they are underpinned by stronger profit growth than the late 1990s.

Still, a new wave of liquidity could drive speculative fervor, pushing equities even higher in the near term.

Bottom Line

The bull market is showing early signs of broadening beyond the Magnificent Seven.

Forward earnings revisions are improving across the S&P 500, and valuations in MidCaps and SmallCaps offer potential upside if earnings accelerate.

Yet risks remain: heavy concentration in mega-cap tech and the possibility of speculative excess fueled by Fed policy.

For investors, this may be a moment to rebalance; trimming exposure to overextended leaders and selectively adding to undervalued segments of the market.

The coming months will reveal whether the bull market evolves into a broad-based rally, or remains a narrow, top-heavy advance vulnerable to shocks.